Financial heavyweights Michael Bloomberg, the founder of Bloomberg LP, and Mark Carney, former governor of the Bank of England, spearheaded the initiative. Larry Fink, CEO of BlackRock, the world’s largest asset manager, warned it would become a requirement for BlackRock’s investments.

Now, the Canadian federal government is making it a requirement for companies that seek funding under the Large Employer Emergency Financing Facility (LEEFF), which will provide bridge financing for large Canadian employers impacted by the COVID-19 pandemic.

The Financial Stability Board’s (FSB) Task Force on Climate-related Financial Disclosures (TCFD or Task Force) is reshaping corporate risk disclosure. We detailed the growing momentum behind sustainability reporting in our last newsletter. We concluded that sustainability reporting is no longer optional for publicly traded companies and there is coalescence around two disclosure standards: TCFD and SASB (the Sustainability Accounting Standards Board). In this blog post, we take a closer look at the TCFD. What is it? What does it say? And how can my company comply?

What is the TCFD?

In 2016, the G20 Finance Ministers and Central Bank Governors became concerned that climate change is a risk that could potentially lead to financial instability. The view was that climate-related risks are one area with inadequate and inconsistent disclosure standards. Precipitous changes in energy use, and the revaluation of carbon-intensive assets, may give rise to concerns regarding an abrupt correction in asset values and financial stability. Given these concerns, the TCFD released its final recommendations report and supplemental materials including:

- Recommendations on disclosing climate-related financial information;

- Guidance on how to implement the recommendations; and

- A technical supplement for developing scenario analysis.

What Does the TCFD Say?

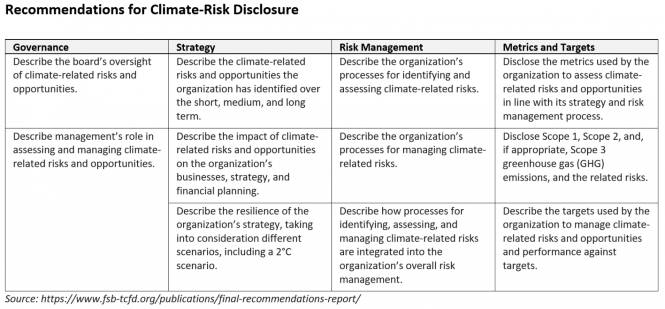

The Task Force structures its recommendations around four key areas (see table below). There are sections asking for details on the organization’s governance practices, the impact that climate changes could have on the company’s strategy, the processes used to manage risk, and metrics/targets used to assess and manage climate risk.

How Can My Company Comply?

Here we outline some of the potential areas where you, the sustainability manager, should take note as you walk your organization through the process of building TCFD-compliant disclosure.

Climate-related risk/opportunities: The Task Force defines specific categories for climate-related risks and opportunities, and encourages organizations to evaluate and disclose those that are most pertinent as part of their financial statement preparation and reporting processes.

Scenario analysis: One of the Task Force’s key recommendations is to disclose potential impacts of climate-related risks and opportunities on an organization’s businesses, strategies, and financial planning under potential future scenarios.

Material risk: The principle of materiality for disclosure of climate-related strategy and metrics and targets can be ambiguous. The TCFD provides recommendations to assist reporting companies with defining material risk.

Alignment: The TCFD helps you with the task of migration by mapping recommendations with other reporting guidance (e.g. CDP, GRI).

Support: To build a robust TCFD-aligned report, we suggest sustainability managers take the following steps:

- Ensure your organization has the proper risk management and governance processes in place.

- Get familiar with the TCFD disclosure guidance and supplemental guidance depending on your company’s sector.

- Seek out gaps in your internal strategy and risk management processes.

- Robust disclosure requires good data. Have the right tools in place to measure and track key climate-related metrics.

- Data allows for risk to be measured. Targets allow for risk to be managed. Think about how your organization will manage climate-related risks and opportunities and how you will show progress against targets.

For additional information or to discuss this topic further, please visit Frostbyte’s website or contact me directly at [email protected].